The Obstacles to Getting to “Yes” With Iran

The ongoing negotiation process between the United States and Iran will be complex and volatile – while some of the most central issues might be soluble, sanctions issues might prove intractable.

When Egyptian President Abdel Fatah al-Sisi confidently addressed Arab Gulf heads of state and foreign ministers and delegates of the Manama Dialogue on Friday, he made no mention of a continued need of Gulf aid and loans to Egypt, instead his remarks focused on regional security cooperation and the preference for Arab state-led intervention in Middle East conflicts.

Help AGSIW highlight youth voices in the Gulf.

DonateWhen Egyptian President Abdel Fatah al-Sisi confidently addressed Arab Gulf heads of state and foreign ministers and delegates of the Manama Dialogue on Friday, he made no mention of a continued need of Gulf aid and loans to Egypt, instead his remarks focused on regional security cooperation and the preference for Arab state-led intervention in Middle East conflicts. Nevertheless, the stability of Egypt may depend on regional financial cooperation and intervention.

Regional finance analysts and foreign currency traders are closely watching the foreign reserve levels of both the Central Bank of Egypt and its local bank sector. Like much of the Gulf bank sector at present, Egypt is facing a period of lower foreign reserve assets. The Egyptian case is of course more severe, as it is increasingly dependent on loans, aid (including in-kind aid of oil and gas), and cash deposits in foreign currency to its central bank from friendly Gulf governments.

Some Egyptian banks are seeking external financing to bridge the gap. Egypt’s two largest banks, National Bank of Egypt and Banque Misr, were not able to complete plans for an international bond issue and instead raised capital through the regional wholesale market with loans totaling several hundred million dollars, according to analysts at EFG Hermes.

For banks with regional parent companies, there is a better cushion for liquidity. Increasingly, large deals requiring foreign currency involve Gulf banks, which is a boost to lagging infrastructure and construction projects inside the Gulf Cooperation Council (GCC). The other big project finance is only possible through companies willing to invest in Egypt by providing their own funding. For example, Siemens has secured a long term finance agreement through export credit agencies in Germany and Denmark, along with regional partners to build a series of electricity plants.

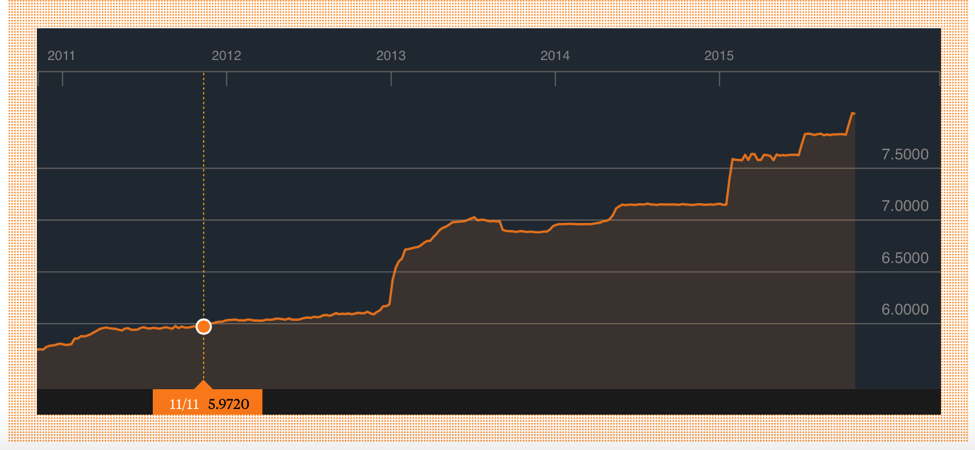

Egypt’s recovery plan depends on infrastructure investment, job creation, housing construction and agricultural development. All of these plans require massive amounts of capital and the local market is not in a position to fund them. The government’s response has been to issue debt denominated in US dollars and Euro (also called “government paper” debt) to increase net foreign assets. Unfortunately, the Egyptian currency continues to weaken, making these liabilities, both public and in the private bank sector, more difficult to repay.

US Dollar to Egyptian Pound Exchange Rate, 2011 to 2015

According to analysts at JP Morgan, Egypt will soon have to repay more than $2 billion in outstanding sovereign debt (including $1 billion in a bond to Qatar, and two payments to the Paris club before July 2016 worth $700 million each.) The question remains if the GCC states will be willing to again replenish (in cash aid and loans) Egypt’s dwindling foreign reserves. A more likely scenario will see GCC support increase in foreign direct investment and regional bank loans, which offers a better promise of return and supports the Gulf economies as much as Egypt’s economy.

The ongoing negotiation process between the United States and Iran will be complex and volatile – while some of the most central issues might be soluble, sanctions issues might prove intractable.

Global demand forecasts by leading agencies have diverged sharply, reflecting a deepening sense of uncertainty about the future path of the global economy.

Trump’s trip to Saudi Arabia has the potential not only to reinforce the deep-rooted U.S.-Saudi alliance but also to expose the fault lines that could undermine future cooperation.

Through its careful examination of the forces shaping the evolution of Gulf societies and the new generation of emerging leaders, AGSIW facilitates a richer understanding of the role the countries in this key geostrategic region can be expected to play in the 21st century.

Learn More

{kind=link}