The Obstacles to Getting to “Yes” With Iran

The ongoing negotiation process between the United States and Iran will be complex and volatile – while some of the most central issues might be soluble, sanctions issues might prove intractable.

Qatar is sharpening its competitive edge in the global gas markets with the lifting of a 12-year moratorium on development at its offshore North Field.

Help AGSIW highlight youth voices in the Gulf.

DonateQatar is sharpening its competitive edge in the global gas markets with the lifting of a 12-year moratorium on development at its prized offshore North Field, the world’s largest gas reservoir. Qatar has long reigned as the world’s largest exporter of liquefied natural gas, but the country is set to lose its dominant market position in the next several years as Australia, the United States, and Russia monetize their growing production of conventional gas and unconventional shale gas with new LNG export capacity.

The LNG trade is forecast to expand by 50 percent by 2020 with a wave of new projects slated to come online over the next several years to meet growing demand. LNG has become the fuel of choice not only because it is clean and efficient, but also because it is a flexible source of supply, particularly where access to natural gas by pipeline may be limited by geographic or economic conditions.

The policy reversal is a shot across the bow to competitors around the world that Qatar intends to remain a giant in the global gas business after its voluntary hiatus, and may prompt companies to reconsider any further plans to raise capacity. Qatar Petroleum’s Chief Executive Officer Saad Sherida Al-Kaabi took the industry by surprise  when he announced on April 3 that the company planned to develop a new project in the southern region of the field that will increase natural gas production capacity by about 10 percent in five to seven years.

when he announced on April 3 that the company planned to develop a new project in the southern region of the field that will increase natural gas production capacity by about 10 percent in five to seven years.

Qatar declared a moratorium in 2005 on the development of the North Field, which it shares with Iran, in order to assess the impact of the rapid rise in output over a short period of time, which can increase the risk of a loss of pressure in the field and cause structural damage. Kaabi said Qatar Petroleum has undertaken extensive technical studies of the field to design the most effective and advanced production strategy for its long-term development and “now is a good time to lift the moratorium.”

Impeccable Timing

Qatar’s decision to further develop the North Field was unexpected, in part because of the current weak LNG market outlook. Also it was widely believed that the country would continue to refrain from sanctioning new, expensive gas projects amid budget constraints in the low oil and gas price environment, as well as competing demands for spending on infrastructure needed for hosting the 2022 FIFA World Cup.

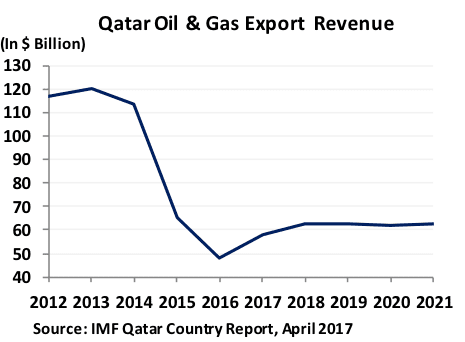

The timing of the decision, however, appears pragmatic and fortuitous for a number of reasons, not least because increased gas production as early as 2022 will provide much-needed incremental revenue to government coffers battered by the three-year downturn in oil and gas prices. By any measure, Qatar is one of the wealthiest countries in the world per capita, possesses gas resources forecast to last at least another 135 years at current production levels, and holds considerable assets through its sovereign wealth fund.

Nonetheless, Qatar’s government is highly dependent on hydrocarbon revenue, even more so than some other Gulf Cooperation Council countries, according to the International Monetary Fund. The average share of hydrocarbon earnings from oil and gas receipts, royalties, and taxes on oil-related activities in government revenue is  around 85 percent. Like other GCC countries, Qatar has turned to debt markets to bridge the fiscal shortfalls brought on by low oil and gas prices. Despite the country’s substantial resources, S&P Global Ratings on March 5 downgraded its outlook on Qatar to negative from stable on concerns that the country’s rising external debt will continue to outpace the growth of its investments internationally.

around 85 percent. Like other GCC countries, Qatar has turned to debt markets to bridge the fiscal shortfalls brought on by low oil and gas prices. Despite the country’s substantial resources, S&P Global Ratings on March 5 downgraded its outlook on Qatar to negative from stable on concerns that the country’s rising external debt will continue to outpace the growth of its investments internationally.

Doha’s financial woes have been further strained by the steep $200 billion spending on infrastructure projects and service industries ahead of the World Cup. The country’s Ministry of Economy and Commerce said the government has embarked on an extensive investment program that calls for “investing oil and gas revenues into major infrastructure projects, manufacturing and to strengthen and develop financial and government services.” The plan also includes substantial investment in the transportation and tourism sectors.

Battle for Market Share

Qatar’s massive North Field gas reservoir was discovered in 1971 but it was not until the 1990s that state-owned Qatar Petroleum partnered with ExxonMobil and Total to pioneer the LNG industry. LNG is the liquid form of natural gas at a cryogenic temperature of −265°F, which condenses the volume by a factor of approximately 600. This reduction in volume enables the gas to be transported economically over long distances in specially designed LNG tankers. Upon arrival at its destination, it is then processed at regasification terminals.

The first exports started in 1997 and within a decade the country was the world’s largest producer of LNG. Total LNG exports reached a record 258 million tons (mt) in 2016, with Qatar capturing one-third of the trade at 77.2 mt, according to the International Gas Union. However, Qatar is set to lose its dominant market position in the next several years as significant new production capacity is brought online in Australia, where LNG exports are forecast to rise from 44 mt in 2016 to around 65 mt in 2017 and 85 mt by 2020. The United States, with its massively expanding LNG industry fueled by rising shale gas, is expected to increase exports from just under 3 mt in 2016 to a staggering 68 mt by 2020-21.

The first exports started in 1997 and within a decade the country was the world’s largest producer of LNG. Total LNG exports reached a record 258 million tons (mt) in 2016, with Qatar capturing one-third of the trade at 77.2 mt, according to the International Gas Union. However, Qatar is set to lose its dominant market position in the next several years as significant new production capacity is brought online in Australia, where LNG exports are forecast to rise from 44 mt in 2016 to around 65 mt in 2017 and 85 mt by 2020. The United States, with its massively expanding LNG industry fueled by rising shale gas, is expected to increase exports from just under 3 mt in 2016 to a staggering 68 mt by 2020-21.

Forecasters have long been arguing that the wave of new LNG export capacity slated to come online between 2016 and 2020 will flood markets and overwhelm demand, placing further pressure on already weak prices. Global LNG export capacity is forecast to rise by 45 percent between 2015 and 2021, with Australia and the United States providing 80 percent of the increase, according to the International Energy Agency. Since mid-2014, Global LNG prices have declined in tandem with oil prices, to which many LNG contracts are indexed. Given this bearish LNG market outlook, few anticipated Qatar would announce plans to increase production.

But, not for the first time, many forecasters have missed the mark. Analysts’ expectations that a surge in new LNG supplies would outpace demand growth in 2016 failed to materialize. Instead, greater than expected demand in Asia, especially China and India, and the Middle East absorbed the increase in supply, which came mostly from Australia, according to Shell’s LNG Outlook 2017. Total new capacity is still on track to increase from 260 mt in 2016 to around 370 mt by 2020. However, predicting an accurate development timeline is fraught with unexpected complications. Indeed, project slippage and lengthy commissioning periods have become a feature of the market.

Moreover, new supply has also been offset by increased demand from new importing countries such as Colombia, Egypt, Jamaica, Jordan, Pakistan, and Poland, replacing declining domestic gas supplies, according to the Shell report. The number of countries importing LNG rose to 35 in 2016, up from around 10 in 2000. LNG demand growth is forecast at 4 to 5 percent a year through 2030, according to the report. Similarly, the IEA forecasts a strong 40 percent increase in Asian LNG demand in the medium term, with imports rising to around 260 mt per year by 2021, up 40 percent relative to the 2016 level. Asia accounts for approximately 75 percent of LNG trade, driven by geographic isolation and scarcity of gas resources. In 2016, Japan, South Korea, China, India, and Taiwan accounted for 70 percent of total imports at 178 mt.

Moreover, new supply has also been offset by increased demand from new importing countries such as Colombia, Egypt, Jamaica, Jordan, Pakistan, and Poland, replacing declining domestic gas supplies, according to the Shell report. The number of countries importing LNG rose to 35 in 2016, up from around 10 in 2000. LNG demand growth is forecast at 4 to 5 percent a year through 2030, according to the report. Similarly, the IEA forecasts a strong 40 percent increase in Asian LNG demand in the medium term, with imports rising to around 260 mt per year by 2021, up 40 percent relative to the 2016 level. Asia accounts for approximately 75 percent of LNG trade, driven by geographic isolation and scarcity of gas resources. In 2016, Japan, South Korea, China, India, and Taiwan accounted for 70 percent of total imports at 178 mt.

Qatar Poised to Fill Looming Supply Gap

Against a backdrop of projected strong demand growth, the global LNG market is expected to tighten after 2020, providing Qatar an opportunity to recapture its dominant role. During the current low price environment companies have deferred investment decisions on new projects, and as a result, additional LNG supply will be needed to meet global LNG demand after 2020. Capital intensive, with long lead times of five to seven years for full development of LNG projects, means final investment decisions will need to be made soon to meet the forecast higher demand after 2020. Currently there are few projects greenlighted to come online after 2022, with the exception of Qatar’s recently announced plans.

Going forward, Qatar has a lower cost advantage over competitors, especially given that Qatar produces significant volumes of condensates and natural gas liquids (NGLs) associated with its natural gas production that provide additional revenue. Qatar already has infrastructure in place that could be expanded to handle increased volumes. For new market entrants, building new greenfield LNG capacity will be considerably more expensive.

Qatar Petroleum has not announced who its new partners will be in the venture but will likely select an existing joint venture company with long experience in the field such as ExxonMobil or Total. The offshore Barzan field, the last big project to be sanctioned before Doha imposed the moratorium, is expected to come online this year after gas leaks delayed the planned start in late 2016, and will add 1.4 billion cubic feet per day (bcf/d) to current production of 17.8 bcf/d. Barzan, owned 93 percent by Qatar Petroleum and the rest by Exxon, is expected to add around 20 percent to pipeline gas production and is earmarked for the country’s power and water sectors. Qatar also exports around 1.9 bcf/d of gas via the Dolphin Pipeline to the United Arab Emirates and Oman. The new project development is expected to add a further 2 bcf/d and push Qatar’s total gas production to a peak of around 21 bcf/d by 2022-24 and ensure the country remains the third largest gas producer in the world, behind Russia and the United States.

Qatar is also the world’s second largest producer of condensates and NGLs, behind Saudi Arabia. Condensate and NGL production is forecast to edge up marginally by 2020, to 1.26 million barrels per day. By contrast, Qatar’s crude production has been slowly edging lower since 2008, with the current strategy aimed at stemming natural decline rates and maintaining existing production levels of around 660,000 barrels per day at the aging fields.

Qatar-Iran Relations

Qatar has been mindful with its production strategy so as not to strain relations with Iran, whose development of the shared field has lagged given the constraints of international sanctions, financial resources, and technology. Qatar controls about two-thirds of the field and Iran holds the remaining one-third, which it calls South Pars. Qatar’s self-imposed moratorium was also considered a necessary move to maintain a positive, constructive political relationship with Tehran, which over the years has had to quell accusations that Doha was “stealing” Iran’s gas.

After years of delays, Iran is on track to surpass Qatar’s output levels this year, which effectively freed Doha to lift its self-imposed ban on production projects in the North Field. Iran has made developing production from South Pars a top priority following the lifting of international sanctions in January 2016. In November 2016 the country signed a preliminary agreement with France’s Total to develop its South Pars II project. Kaabi said Iran’s plans to further develop South Pars were not a factor in Qatar’s decision to lift the moratorium but nonetheless will help close the projected gap in output. “What we are doing today is something completely new and we will in [the] future of course … share information on this with [Iran],” Kaabi said.

Iran is hoping to increase production at South Pars to 28.1 bcf/d once it completes its planned 24 phases of development sometime in the middle of the next decade. However, unlike Qatar, which exports most of its gas as LNG, Iran’s higher gas production is needed to meet growing domestic demand, as well as for reinjection into aging oil fields and for industrial projects.

For Qatar, the supply, demand, and political dynamics have now aligned to enable the country to lift the moratorium and position itself for future growth in LNG capacity that will ensure it recaptures its top exporter role in the coming decade. Equally, Qatar’s rich natural gas resources and status as the world’s largest LNG exporter have enabled Doha to exert considerable independence and political influence in the region that belies the country’s small size, a lofty position the government wants to maintain.

The ongoing negotiation process between the United States and Iran will be complex and volatile – while some of the most central issues might be soluble, sanctions issues might prove intractable.

Global demand forecasts by leading agencies have diverged sharply, reflecting a deepening sense of uncertainty about the future path of the global economy.

Trump’s trip to Saudi Arabia has the potential not only to reinforce the deep-rooted U.S.-Saudi alliance but also to expose the fault lines that could undermine future cooperation.

Through its careful examination of the forces shaping the evolution of Gulf societies and the new generation of emerging leaders, AGSIW facilitates a richer understanding of the role the countries in this key geostrategic region can be expected to play in the 21st century.

Learn More